When you turn 65 and enroll in Medicare, one of the first decisions you face is how to fill in the gaps that traditional Medicare leaves. Parts A and B cover hospital and outpatient care, but they leave you exposed to significant out-of-pocket costs — deductibles, coinsurance, and no cap on what you could owe in a bad health year. The two main approaches to managing that exposure are Medicare Advantage and Medigap. Both are widely used and both solve real problems, but they do it in fundamentally different ways, and the choice between them has long-term implications that are easy to underestimate at enrollment.

This is not a decision to make based on premium alone. The right choice depends on your health situation, how you use healthcare, where you live, your financial resources, your travel habits, and — critically — your willingness to accept uncertainty about future health needs in exchange for lower current costs.

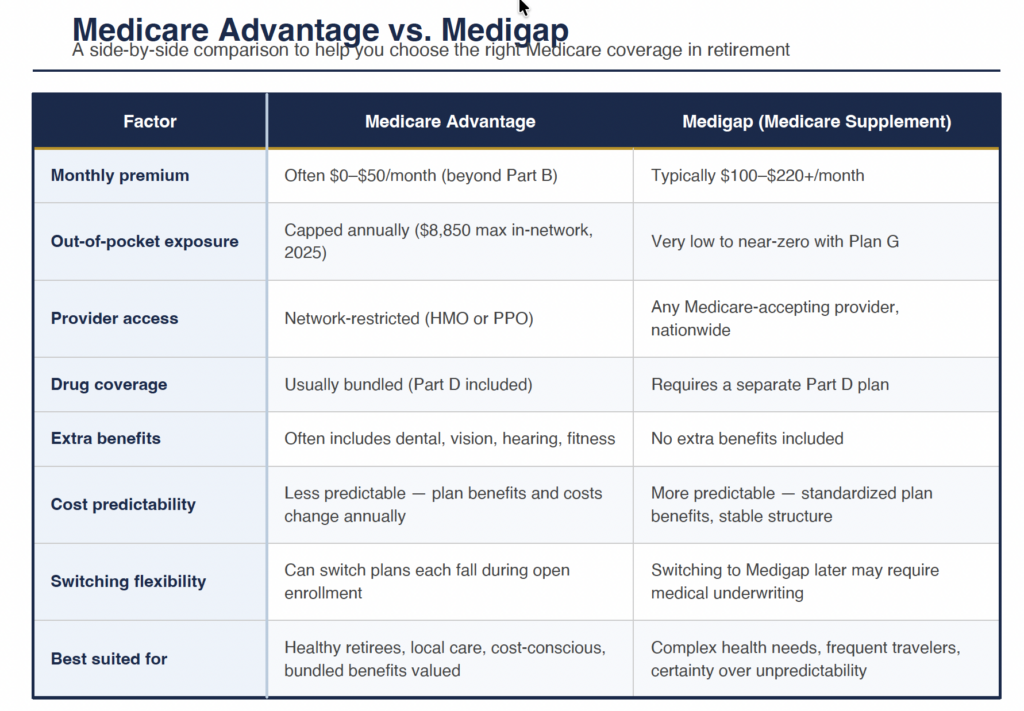

How Traditional Medicare Works — and Why the Gap Exists

Traditional Medicare Part A and Part B provide meaningful coverage, but they were designed decades ago with a cost-sharing structure that transfers significant financial risk to the beneficiary. Part A has a per-benefit-period hospital deductible (over $1,600 in 2025) with daily coinsurance for extended hospital stays. Part B has an annual deductible and then covers 80 percent of approved costs — leaving you responsible for the remaining 20 percent with no out-of-pocket maximum.

That 20 percent with no cap is the core problem. A serious illness or hospitalization under traditional Medicare alone can generate five- or six-figure out-of-pocket costs. Neither Medicare Advantage nor Medigap eliminates all of that exposure, but each addresses it in its own way.

What Medicare Advantage Is

Medicare Advantage — officially Medicare Part C — is a private health insurance plan approved by Medicare that replaces your traditional Medicare coverage. Instead of Medicare paying your claims directly, you receive your Medicare benefits through the private plan, which typically operates as an HMO or PPO network.

Most Medicare Advantage plans include Part D drug coverage and often bundle additional benefits like dental, vision, hearing, and fitness programs that traditional Medicare does not cover. Many plans have low or even zero monthly premiums beyond what you already pay for Part B. The tradeoff is that you receive care within the plan’s provider network and the plan’s own cost-sharing structure — copays, coinsurance, and an annual out-of-pocket maximum — rather than Medicare’s original structure.

The out-of-pocket maximum is the most important financial protection Medicare Advantage offers. In 2025, the maximum allowed by law is $8,850 for in-network costs. Once you hit that ceiling in a calendar year, the plan covers 100 percent of additional in-network costs for the remainder of the year. This is a meaningful cap that traditional Medicare alone does not provide.

Medicare Advantage plans vary significantly by carrier, county, and year. Networks change. Benefits change. Premiums and cost-sharing structures change annually during the open enrollment period in the fall. A plan that is a strong fit in year one may look quite different in year three.

What Medigap Is

Medigap — also called Medicare Supplement insurance — does not replace traditional Medicare. Instead, it works alongside Parts A and B to pay most or all of the cost-sharing that Medicare leaves behind: the Part A hospital deductible, the Part B coinsurance, and in some plans the Part B deductible. You keep your traditional Medicare coverage and your Medigap policy pays second, filling in the gaps.

Medigap policies are standardized by federal law into lettered plan types (Plan G and Plan N are the most commonly purchased today). The benefits of a given plan letter are identical regardless of which insurance company sells it — Plan G from Carrier A covers exactly the same things as Plan G from Carrier B. What differs between carriers is the monthly premium and, to some degree, financial stability and customer service. This standardization makes Medigap comparatively straightforward to shop.

The most significant feature of Medigap is unrestricted provider access. Any provider who accepts Medicare accepts your Medigap policy. There are no networks, no referrals required, and no prior authorization for most services. If your doctor accepts Medicare, you can see them. This is particularly valuable for people with established specialist relationships, for frequent travelers, or for anyone who wants the freedom to seek care at major medical centers or out of state without worrying about network coverage.

Medigap premiums are higher than Medicare Advantage premiums — often substantially so, particularly at older ages. Plan G premiums for a 65-year-old in California commonly range from $100 to $200 or more per month depending on the carrier and rating method. Premiums typically increase with age (under attained-age rating) or at scheduled intervals (under issue-age or community rating). The premium stability of the plan type and the rating methodology of the carrier you choose matters significantly over a 20- or 30-year retirement.

The Core Tradeoffs — A Direct Comparison

The decision ultimately comes down to a set of specific tradeoffs. Neither plan type is universally better — the right answer depends on which tradeoffs matter most to your situation.

The Underwriting Problem — Why Switching Later Is Harder Than You Think

This is the single most important factor that people underestimate when they choose Medicare Advantage at 65 because the premium looks attractive.

When you first enroll in Medicare at 65 and choose Medigap during your Initial Enrollment Period, you have a federally guaranteed right to purchase any Medigap plan offered in your state at standard rates — regardless of your health history. Insurers cannot deny you coverage or charge you more because of pre-existing conditions during this window.

If you choose Medicare Advantage at 65 instead and later want to switch to Medigap — perhaps because your health has changed, your preferred doctors left the network, or you want more coverage certainty — you will in most states face medical underwriting. The insurer can review your health history, charge higher premiums based on conditions you have developed, or deny you coverage entirely. California has somewhat stronger protections than many states in certain circumstances, but the general rule applies: the guaranteed-issue window at 65 is the easiest and cheapest time to get Medigap. Waiting makes it harder and potentially much more expensive.

This asymmetry is the central risk of choosing Medicare Advantage primarily for its lower upfront premium. If your health stays excellent, the lower premium may indeed be the better outcome. But if your health changes — which is a reasonable expectation over a 20-year retirement — you may find yourself wanting Medigap coverage at exactly the time when getting it has become difficult or prohibitively expensive.

Who Medicare Advantage Tends to Work Well For

Medicare Advantage is often a strong fit for retirees who are in good health at enrollment and expect to remain so, who receive most of their care locally from providers within a predictable network, who value the bundled extra benefits (particularly dental and vision), and who are comfortable with the annual plan selection process and the possibility of adjusting their plan each fall.

It also tends to work well for retirees with tighter budgets for whom the premium difference between Advantage and Medigap represents a meaningful monthly constraint, and who are willing to manage the network and prior authorization requirements that come with an HMO or PPO structure in exchange for that lower cost.

California has a competitive Medicare Advantage market with many plan options, particularly in urban and suburban areas. Rural areas typically have fewer plan choices and narrower networks, which can limit the appeal of Advantage plans for retirees outside major metro areas.

Who Medigap Tends to Work Well For

Medigap tends to be the stronger choice for retirees with chronic conditions or complex health needs where ongoing specialist access and cost predictability matter, for those who travel frequently or split time between states, for retirees with established doctor relationships they do not want to put at network risk, and for people who place high value on the certainty of knowing their out-of-pocket costs will remain very low regardless of what health events occur.

It is also the better structural choice for retirees who are thinking about their coverage over a 20- or 30-year horizon. The guaranteed-issue window at 65, the standardized plan structure, and the freedom from network restrictions all become more valuable over time as health needs typically become more complex and the ability to see specialists at major medical centers becomes more important.

For higher-income retirees for whom the premium difference is not a budget constraint, Medigap’s combination of comprehensive coverage, provider freedom, and predictability is generally the more rational long-term choice — even if Medicare Advantage offers lower apparent costs in the short run.

The CalPERS Retiree Health Benefits Context

For California retirees who qualify for CalPERS retiree health benefits, this decision has an additional layer of complexity. CalPERS offers Medicare-coordinating health plans for retirees who are Medicare-eligible, and in some cases the CalPERS group coverage can provide benefits comparable to Medigap at costs that are difficult to match in the individual market. CalPERS members approaching Medicare eligibility should evaluate their CalPERS post-retirement health options alongside the individual Medicare Advantage and Medigap market rather than treating them as separate decisions.

Practical Steps for Making the Decision

The decision does not need to be made in the abstract. A structured comparison process makes it tractable.

- Start with your doctors. Identify the providers you currently see or expect to see in retirement. Check whether they participate in the Medicare Advantage plans available in your county. If your most important relationships are not in network for the plans you are comparing, the premium advantage of Advantage may not be worth the disruption.

- Get actual plan quotes. Use the Medicare Plan Finder tool at medicare.gov and contact two or three Medigap carriers for Plan G and Plan N quotes in your zip code. Compare the total annual cost — premium plus likely out-of-pocket — under both approaches given your anticipated healthcare use.

- Think about your health trajectory. Be honest about your family history, current conditions, and long-term health expectations. If there is meaningful probability that your health needs will become complex, the long-term value of Medigap’s guaranteed access and predictability goes up.

- Consider the switching asymmetry explicitly. Ask yourself: if I choose Medicare Advantage now and want to switch to Medigap in 10 years, can I realistically do that? The answer in most states is that you may not be able to, or it will cost significantly more. Factor that risk into the comparison.

- Review the IRMAA interaction. Neither Medicare Advantage nor Medigap changes your IRMAA surcharge — that is determined by your income, not your plan type. But the total Medicare cost picture (IRMAA surcharge + Part B premium + plan premium + out-of-pocket) is worth modeling across both scenarios, particularly if you are in or near an IRMAA bracket.

FAQ: Can I Switch From Medicare Advantage to Medigap Later?

In most states, switching from Medicare Advantage to Medigap after your guaranteed-issue window at age 65 requires passing medical underwriting — meaning the insurer can review your health history, charge higher premiums based on conditions you have developed, or deny coverage entirely. California has some additional consumer protections that provide limited guaranteed-issue rights in specific circumstances (such as certain plan discontinuations), but these are narrower than the full guaranteed-issue rights you have at initial enrollment. The practical implication: if you are considering Medigap at all, evaluating it seriously at age 65 — rather than defaulting to Medicare Advantage and planning to switch later — is almost always the better approach. Switching into Medigap from a healthy baseline is straightforward. Switching in after a significant health event is much harder and potentially not possible at standard rates.

The Medicare coverage decision you make at 65 tends to shape your healthcare experience — and your out-of-pocket exposure — for decades. It deserves the same deliberate analysis as any other major retirement planning decision.

Schedule a complimentary Medicare planning consultation with our office. We will walk through the Medicare Advantage and Medigap options available in your area, compare the total cost picture against your health history and retirement plans, and help you make a coverage decision you can feel confident about — not just at 65, but throughout your retirement.